7 Money Rules You Need to Build Financial Health

Managing your money can be overwhelming, especially when you’re not sure where to start. That’s why having a set of money rules can help you make sound financial decisions and achieve long-term financial stability.

Personal finance expert Ramit Sethi from the book “I Will Teach You to Be Rich” has his own 10 Money Rules that he follows to navigate his life.

I’ve built my own set of 7 money rules myself to help me ensure that I use money as a tool in my life.

Having a set of money rules allowed me to define my relationship with money and how to use money to create my optimal life.

“Spend extravagantly on the things you love, and cut costs mercilessly on the things you don’t.” – Ramit Sethi

There are 7 money rules that I’ve set for myself to build a strong financial foundation.

You can use these rules as a guideline, but make sure to tweak and tailor them to fit your own life, values, and priorities.

My 7 Money Rules

-

- Asking how can I afford this instead of thinking “I can’t afford this.

- Always have a 3-month emergency fund in cash

- No limit on spending related to health, education, & safety

- Invest in quality items and keep them for as long as possible

- Think about the ROI, Opportunity Cost, and MU of each purchase

- Avoid credit card debt

- Save 10% & Invest 20% of your annual income

1. Asking “How can I afford this?” instead of thinking “I can’t afford this.”

The way you think about money can have a big impact on your financial decisions. Instead of feeling limited by your budget, try to approach every purchase with a problem-solving mindset.

By asking “How can I afford this?” you’ll be more likely to find creative solutions to make your money work for you.

Working hard to shed your limiting beliefs about money will help you reach your financial goals faster.

2. Always have a 3-month emergency fund in cash.

Having an emergency fund is crucial for financial stability. I recommend keeping at least three months’ worth of living expenses in a separate savings account that is easily accessible in case of an emergency.

I feel more comfortable having a year’s worth of emergency funds on hand, but this is also because I do not feel very secure in today’s job market. This number could change for me later on once the economy improves.

To avoid dipping into your emergency fund, you can create sinking funds to prepare for irregular expenses.

3. No limit on spending related to health, education, & safety.

When it comes to your health, education, and safety are almost always worth spending money on.

It’s important not to put a price tag on your well-being. Your health and safety should always be a top priority as these two factors will directly impact the quality of every experience in your life.

I used to be very reluctant to spend money on Ubers. But as a small Asian girl living in a (very unsafe) big city, I came to accept that I need to be ok with spending money on Ubers if I end up staying out late.

Money is useless if you are not healthy and alive.

Education should also be an area where you are constantly investing in.

Your education is a deciding factor in how much money you’ll make in your lifetime. It’s important to keep learning high-income skills.

4. Invest in quality items and keep them for as long as possible.

In today’s consumer culture, it’s easy to fall into the trap of buying cheap, disposable items.

However, investing in quality items that will last for years can save you money in the long run.

By choosing well-made products, you’ll avoid the cost and hassle of constantly replacing low-quality items.

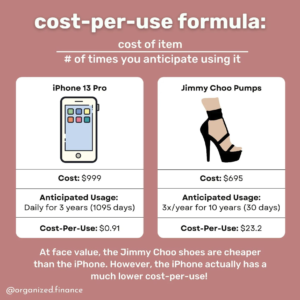

You can calculate whether or not an item is worth buying by thinking about the item’s Cost Per Use instead of just looking at the price tag.

Cost Per Use = Cost of Item / Number of Times You Will Use It.

Here is an example by Organized Finance demonstrating how to use the Cost-Per-Use formula.

5. Think about the ROI, OC, and MU of each purchase.

Before making a purchase, it’s important to consider the return on investment (ROI), the opportunity cost (OC) of not using that money elsewhere, and the marginal utility (MU) of the purchase.

-

- Return on Investment (ROI): Profitability of an investment compared to its cost

-

- Opportunity Cost (OC): Loss of potential gain from other alternatives when one alternative is chosen

-

- Marginal Utility (MU): Satisfaction or benefit gained from consuming a good or service

This rule allows me to spend intentionally and helps me make more informed decisions about how to spend money.

It allows me to understand exactly why I want to make a purchase or investment and what I am giving up when I spend money.

Considering something’s ROI applies when I am looking into investments – whether it’s investing in a tool, a class, or an asset like stocks – to see if the investment is worth it. An investment could be pricey upfront, but it would be worth it if it will yield high returns in the future.

Opportunity cost is the idea of giving up something to get something else. For example, if I spend $5 a day on coffee, I’m giving up $150 a month that I could invest in stocks, which would be worth over $26K in 10 years due to compounding interest (assuming 7% annual returns). Considering the opportunity cost forces me to think about the potential gain I am sacrificing when I choose to spend my money.

Thinking about the long-term marginal utility of something makes me more intentional with my spending when it comes to short-term items or material goods.

It is easy to get influenced by marketing and make impulse buys, but it is important to consider whether I really need or just want the item. Sometimes we turn to retail therapy and experience buyer’s remorse, so taking 48 hours to think about a purchase also allows me to combat impulse buying.

6. Avoid credit card debt.

Credit card debt can be a major financial burden, thanks to high-interest rates and fees.

Whenever possible, avoid using credit cards for purchases that you can’t pay off in full each month. Always make sure you are following credit card best practices to stay out of debt while you rack up those points and rewards.

Getting into the habit of paying your credit card in full every month will also allow you to you keep your credit score high!

7. Save 10% & Invest 20% of your annual income.

Finally, saving and investing are key components of building long-term financial stability. I recommend saving at least 10% of your annual income in a separate savings account and investing at least 20% in a diversified portfolio of stocks, bonds, and other investments.

Building Your Own Rules

By following these 7 money rules, you can build a strong foundation for your financial future.

Remember, managing your money is a journey, and it’s important to be patient and stay committed to your goals. These are the rules that work for my lifestyle.

Make edits as needed depending on your specific life situation.

With these rules as your guide, you’ll be well on your way to achieving financial stability and success.